- 1. Advice on How to Save Money for a Baby

- 2. Financial Planning Before a Baby

- 3. Ongoing Costs

- 3.1. Kid Care

- 3.2. Necessities

- 3.3. Clothing

- 3.4. The Doctor

- 3.5. In the first year, the budget was for six wellness visits for vaccinations, exams, and other purposes, as well as a few extra visits for illnesses.

- 3.6. For your rates, check your health insurance policy. If you do not have enough money, you can always turn to the Child Care and Development Fund, which can help you with many financial issues.

- 3.7. Diapers

- 3.8. Food

- 4. Conclusion

Being a parent should mostly cause excitement and delight, but it’s reasonable to feel a small amount of stress, especially when you consider the baby’s budget.

Before you learn how to create a budget and deal with other parenting-related financial issues, take into account the following: Your financial situation will continue to change for years after becoming a parent.

You may expect a rough ride. Be composed. The keys to creating a budget for motherhood are flexibility and readiness in equal measure.

Advice on How to Save Money for a Baby

Building a budget with goals, adhering to that budget, and planning for unforeseen costs are all part of learning how to start saving money for a baby.

While there are certain continuing expenses you can depend on, like food and diapers, you’ll often run into crises that you hadn’t planned for. Take into account the following recommended practices as you get ready for the unexpected:

Establish an Emergency Fund

Put money aside for emergencies as you begin to budget for your newborn. This kind of fund should typically last between three and six months, but even beginning small and adding to it with each paycheck can benefit you in the long term.

If you have debts, then it is better to start thinking about paying them off or consulting with the best debt consolidation companies so that loans do not interfere with the family budget.

Set Financial Priorities

If it isn’t practical to put money into each savings account each month, think about your financial priorities.

Adjust your financial objectives before and throughout your pregnancy so that paying off debt comes first, followed by setting up an emergency fund, and then opening college and retirement accounts.

Save Money

The sooner you begin living on a limited budget, the more equipped you’ll be for when your child is born. Practice living on a single income or an income that is less than your existing family income in the third trimester to get acclimated to a budget that will undoubtedly be reduced.

Financial Planning Before a Baby

Many first-time parents purchase more than they “need.” A very good rug, a cool rocking rocker, or some adorable photographs to display in the nursery may be something you’d want.

That’s great; just make sure you purchase these items after setting aside money for the necessities like food and diapers.

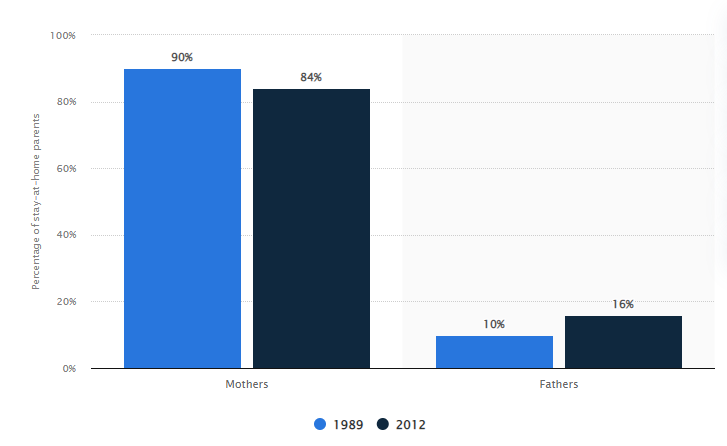

Moreover, if you, like 20% of parents, are a householder, then it is better to save on unnecessary things.

Percentage of stay-at-home parents in the United States in 1989 and 2012, by gender

Link: https://www.statista.com/statistics/319721/percentage-of-stay-at-home-parents-in-the-us-by-gender/

The bare necessities don’t have to be costly, particularly items like clothing or strollers that you may obtain at your neighborhood resale store or via family or friends.

You will need the following items for your newborn:

- Crib

- Dresser

- Auto seat

- Stroller

- Watch for babies

- Clothes

- Diapers

- Food

- Toys

Once you have made the necessary purchases, you may want to think about purchasing the following items for your newborn:

- Changing desk

- Swaying seat

- Playpen

- Sling/carrier

- The diaper bin

- Pacifiers

- A nursery rug

- Added toys

- Nightlight

- White noise generator

Ongoing Costs

The ongoing costs of raising a child begin as soon as your infant is born. Consider including the following expenditures in your budget:

Kid Care

Child care will be your single greatest budget item if both you and your spouse will be working after the birth of your child. The cost of child care depends on many factors, including the age of your child, how much care you need, the kind of care you use, and your location.

The average annual cost of an in-home caregiver, such as a nanny, is about $30,000. However, charges might vary based on variables like geography and other considerations.

However, bear in mind that certain costs, like the credit for daycare costs, may be reimbursed by tax credits. Ensure that you confirm your eligibility.

Necessities

Food, including baby formula, clothing, and diapers make up the majority of recurrent requirements expenses.

Clothing

According to the USDA’s most recent The Cost of Raising a Child study, expecting parents should set aside $650 to $1,100 for clothing over the first two years.

The lowest end is about $55 per month, while the amount may change significantly based on personal preferences and spending power.

The Doctor

In the first year, the budget was for six wellness visits for vaccinations, exams, and other purposes, as well as a few extra visits for illnesses.

For your rates, check your health insurance policy. If you do not have enough money, you can always turn to the Child Care and Development Fund, which can help you with many financial issues.

Diapers

Experts advise saving at least $1000 for diapers and $450 for wipes for the first year alone, even if diaper prices might vary.

This is roughly $120 every month. Parents who want to use disposable diapers for their children should plan to use up to 3,500 diapers in the first year alone.

Food

Once you begin feeding your child substantial meals, you should set up around $120 each month. The costs associated with early meals for children are rather minimal when compared to what you could see from a teenager.

Conclusion

Children are a beautiful gift, although sometimes a costly one. The most important thing to remember is that averages are meaningless when the variation is as vast as it is for expenditures associated with babies.

The majority of your hospital expenditures may be avoided with good health insurance, but the remaining expenses can only be managed with careful planning and budgeting.

Finland’s tradition of providing new parents with a simple starter kit that doubles as a crib shows that many of the tens of thousands of dollars we spend on our kids’ early years are more for our reputation than for their wellbeing.